Последний отзыв

Классная книга. Очень многое объясняет, что скрытое реально происходит в человеке

По всем вопросам обращайтесь на: info@litportal.ru

(©) 2003-2024.

✖

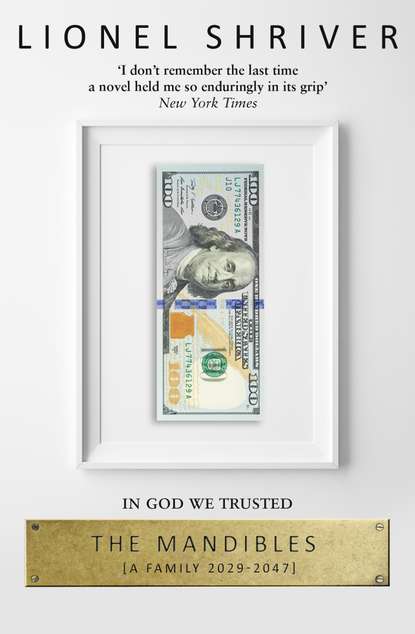

The Mandibles: A Family, 2029–2047

Автор

Год написания книги

2019

Настройки чтения

Размер шрифта

Высота строк

Поля

“Insofar as it’s possible, with no in-depth coverage, no fact-checking—”

“The end of the New York Times,” Douglas said patiently, “was not the end of the world. We all miss it, Carter. But it became a shadow of its former self.”

“Meaning when I worked for it.”

“Tetchiness doesn’t suit you. Aren’t you over seventy?”

“Not yet.”

“But old enough to realize that the end of the world takes place on rather a larger scale. As you must have begun to appreciate. Quite a week!”

“Well”—Carter took a deep breath—“with the stock exchange shut down, I guess you’ve had something of a vacation.”

“If having the federal government deny you access to your own accounts—scarcely different from being locked out of your own house—well, if that’s your idea of a vacation, yes. It’s been all beach umbrellas and boat drinks.”

“And do you know, ah—I mean, ballpark, what kind of a hit you’ve taken?” His father played his financial cards close to his chest. Carter had no idea of the size of the portfolio, down to the number of zeros.

“Use your head. Trading closes automatically once the market dives a set percentage or point drop. The SEC hasn’t deigned to re-open the Exchange since the Level 3 circuit breaker kicked in on Thursday. It doesn’t take much imagination to picture what will happen to the market when they do. I’m sure the SEC has pictured it. So whatever the values at which stocks left off are academic. The question is not what they are worth, but what they will be worth three seconds after the bell. Imagine all those investment-bank computers primed at the starting line—with which my poor fleXcreen can’t compete. Of course, one could argue that the value of assets to which you are denied access, perhaps indefinitely, is zero.” Reseated at a jaunty angle, Douglas had assumed a whimsical demeanor. He seemed almost pleased.

“One could argue?” said Carter. “Or that’s what you’re saying?”

“One could also argue,” Douglas continued with an infuriating mildness, “as a contingent on the web is already promoting, that this is an extraordinary and irrational hysteria from which the market will promptly bounce back. After a historically unprecedented dip, about which academics like your son-in-law will produce miles of trying analytical text, the dollar and the market may both more than recover. In which case, the next month or so could provide a once-in-a-lifetime opportunity to buy low and sell high. With a bit of leveraging, investors swimming against the tide could easily grow their holdings by three or four times.”

This was not the multiple choice for which Carter had made this journey: his father was (a) destitute; (b) rich and about to get a whole lot richer; (c) somewhere in-between. Thanks.

“They’ve put limits on withdrawals, you know,” Carter said sulkily. “I can’t get more than three hundred bucks from an ATM.”

“They’re afraid of more bank runs. By trying too hard to prevent them, more bank runs are exactly what they’ll get—should they ever be so imprudent as to let you at your own money again.”

“The Fed chief was emphatic. Krugman said the limits were for a few days, max.”

“Anyone in a position of authority telling you something unpalatable is ‘temporary’ is a red flag. The quick fix of capital controls can seem so alluring: ‘We’ll simply make the rabble keep their money here. We’ll pass a law!’ The hard part is lifting capital controls, which becomes unthinkable the moment they’re instituted. Who wants to keep funds in a country that confuses a bank account with a bear trap? The moment you remove the constraints, the nation is broke. So you can be sure that at least the freeze on making monetary transfers out of the US will stay in place for some time to come. Look at Cyprus. The capital controls levied in 2013 weren’t entirely rescinded until two years later. Know how long those controls were meant to stay in place at their inception? Four days.”

“But this is the United States. Here, they can’t—”

“They can. And will. There’s nothing the Fed can’t do.” Again, this cheerfulness. Douglas fished a steamer from an inside pocket. The family patriarch was once a two-pack-a-day smoker, and Carter blamed electronic cigarettes for the man’s now-catastrophic longevity. The e-bacco emitted a teasing scent of French vanilla.

“Why do you seem to find this debacle so entertaining?”

“What does it matter if I’m entertained? After all, wasn’t it interesting,” Douglas supposed, stabbing the air with his stainless-steel wand like a Philharmonic conductor, “when the ECB, Japan, the Bank of England, and the Fed banded together to intercede the day after the rate spike, and all that doing ‘whatever it takes to support the dollar’ backfired? Traditionally, investors bow to the inevitable when central banks move in. But rampant purchasing of US securities meant the Fed was conjuring up yet more money out of thin air to buy the bonds. Which is why the dollar tanked in the first place. Made the fire sale of the dollar infinitely worse. I love it when by-the-book remedies don’t work the way they’re supposed to.”

“But you don’t seem the slightest bit upset! Is it because you’re practically a hundred? And there’s not much time left for you? Because not only am I planning to stick around a few more years, but I have kids, and they have kids—”

“Right now, every major stock exchange in the world has halted trading. It’s relaxing. You should enjoy the respite. Because Quiet Time won’t last.”

Finally Carter plunked into the adjoining armchair, doubling his chin on his clavicle with a scowl. He should remember: for the time being, he and his father were on the same side. “Economics isn’t my bailiwick. I don’t understand this ‘bancor’ business. The American news coverage is so hostile that I can’t make heads or tails of it. Guests on CBS just start shouting.”

“I suspect it’s a good idea—if it was not a good idea for Putin to roll it out.”

“At least these days Mr. President for Life keeps his shirt on.”

“I’m intrigued by how a whole new international currency was ready to go. Not the sort of thing one works out on the back of an envelope.”

“Maybe I’d expect a financial putsch from Russia and China,” Carter said. “But this coup is by US allies, too. Okay, not Europe—and never mind them—but the Saudis, the Emirates, Korea—after the tens of billions we shifted to them after unification? Ingrates. Not to mention Brazil, India, South Africa. Even Taiwan! Everyone’s ganging up on us! What’s going on?”

“We should be grateful,” Douglas said. “You do realize that without the bancor lined up as a replacement reserve currency, the fall of the dollar would plunge the entire world economy into a Dark Ages? We’d be buying eggs with rocks.”

“But how can they simply announce that oil, and gas—the whole commodities market—is henceforth to be conducted in these goofball ‘bancors’? It’s our damn oil, too, and our damn corn.” A New York Democrat really shouldn’t be spouting this indignant, nationalistic bilge. Too much American twenty-four-hour news, all singing the same apoplectic tune. Besides, father and son had chosen parts at the start. Douglas had co-opted the voice of reasonableness and fairness, which left Carter to fume.

“A better question is how we’ve got away with shoving our currency down the rest of the world’s throat for so long,” Douglas observed. “It’s been a multipolar world for decades. After the refunding of Social Security, the US defense budget won’t buy a cap pistol. Why should commodities be traded internationally in dollars?”

“Big whoop, you call it a bancor instead of a dollar. Like this ‘New IMF’: semantics.”

“Not just semantics. New means administered by a consortium of countries that presently doesn’t include us.”

“What, is it just, presto!” Carter flailed. “And the dollar is worth zip?”

“Theoretically, the US could buy into the bancor along with everyone else. But only by ponying up real assets to back it. That’s the difference in a nutshell. To swap fiat currency for bancors, you have to fork over to the New IMF a strictly proportioned basket of real commodities—corn, soy, oil, natural gas, deed to agricultural land. Rare earths … copper … Oh, fresh water sources! And gold, of course.”

“No way is Fort Knox moving to Moscow.”

“I don’t expect Washington to play ball. It’s too humiliating. Though if it makes you feel any better? The likes of Indonesia and Pakistan may have leapt to embrace the bancor as an antidote to chaos, but this new regime is going to screw plenty of the very governments that are backing it to the hilt. There’s modest flexibility built in, to avoid another euro debacle. Countries who’ve merely pegged their currencies to the bancor can appeal for devaluation. But the NIMF is bound to be stringent on that point. Since the whole idea of the bancor is to restrict the money supply. From the 1970s, the G-30 have all been churning out Monopoly money as if drawing from a board game with the combined components of several sets. It’s going to ferociously mess with some heads that now you have to cover your expenses and pay your trading partners in a currency that has real value.”

“The whole thing stinks to high heaven. Maybe Putin and his new friends were passively waiting for an opportune moment to pounce. But it’s a hell of a lot more likely that they caused the crash of the dollar.”

“Oh, that’s certainly how the White House is playing it. Big conspiracy. Threat to national security. Nothing to do with a Congress that won’t rein in entitlements. Nothing to do with the deficit, or the national debt, or a monetary policy modeled on the population’s waistline. Only evil outside forces conniving to destroy the greatest country in the world.”

Carter raked his fingers through what remained of his hair; the gene for male pattern baldness being handed down from the mother was a formula for father-son resentment. “I don’t understand how this happened.”

“Carter. I will let you in on what isn’t a secret to any housewife who’s bought a cucumber. The American dollar is worthless now not because of the rate spike, and not because of crashing on the international currency exchange, and not because of the bancor. It is worthless now because it was worthless before.”

“That’s melodramatic.”

“Not melodramatic—dramatic. In the hundred years following the establishment of the Federal Reserve in 1913, the dollar lost 95 percent of its value—when one of the purposes of the Fed was to safeguard the integrity of the currency. Great job, boys! Ever wonder why no one talks about millionaires anymore—why no one but a billionaire rates as rich? Because a man who had about ten grand in 1913 would be a millionaire a century later. Hell, everyone’s a millionaire these days, every halfway solvent member of the middle class. And the majority of that currency decay is historically recent. Why, the dollar lost half its value in the mere four years between 1977 and 1981.”

Never a science-fiction fan, instead Douglas now immersed himself in the more recently minted genre of apocalyptic economics, rehearsing debt-to-GDP ratios as he had once memorized Saul Bellow. (When younger, Carter had never imagined he’d grow nostalgic for being quoted to death from Seize the Day.) If Pop couldn’t remember the age of his only son, the chances were poor that any of this pontificating tutorial was even ballpark accurate. What few scraps of his feverish reading that the old man did recall verbatim would be exaggerated for effect. Yet the last Loony-Tunes statistic was the limit.

“You might double-check that,” Carter chided gently, in preference to what a load of crap. “In 1981, I was a junior in college. Why wouldn’t I remember my own currency that steeply in freefall?”

“Because it’s boring, son. The American government counts on your being bored by it. Why, I barely remember the fallout from Nixon going off the gold standard myself. I buried my head in books. Perhaps the wrong books, looking back, but it’s too late now. The point is, when you’ve debased your currency that utterly, there’s not much further left for it to fall. Besides the sheer dullness of it all, the dollar sliding to the penny hasn’t been all that noticeable because every other government has been busy doing the same thing—running the printing press overtime on the justification that a junk currency advantages exports. The world is drowning in worthless paper. But America in particular has been getting away with murder—playing on the heartbreaking international belief in Treasury bonds as the ultimate ‘safe haven.’ Really, the blind trust bears all the irrational hallmarks of theology. What else, financially, is there to believe in besides the full faith and credit of the United States? So we’ve borrowed for basically nothing on the basis of a childlike credulity for thirty years. You know the Fed’s been steadily trying to monetize the debt—”

“Cut it out, Pop. You’re showing off.” In the agency days, Douglas Mandible held forth about anastrophe, metonymy, and onomatopoeia—and now it was all arbitrage, margin calls, and open market operations. Day trading had infected his father’s mind like a fungus.

“You try living to ninety-seven with a wife who can’t recognize a fork. You’d acquire new expertise out of desperation, too. And it’s not complicated. Why, I taught Willing about monetizing the debt the last time you brought Florence up here, and the kid got it right away. Though I have to say that boy’s got a knack. Has that sharp-eyed, quick-on-the-uptake quality that was obvious in Enola by the time she was three.”

Drawing on an inhuman self-control, Carter stifled, Oh, give me a break!

“So,” Douglas continued. “You loan me ten bucks. I photocopy the bill four times, give you back one of the copies, and announce that we’re square. That’s monetizing the debt: I owe you nothing, and you’re stuck with a scrap of litter. For years, the fact that one can swap dollars for tangible goods and services has been a miracle of God. Why do you think I’m invested in the market? In theory, stocks entail owning real things. Unfortunately, I didn’t take into account that most of those stocks are denominated in dollars. And I’ve been as vulnerable as the next idiot to the bias that keeping the majority of your funds in American companies is erring on the safe side. So I do apologize. Had I any idea what was in the offing, I’d have diversified quite differently.”

Другие электронные книги автора Lionel Shriver

Последний отзыв

Классная книга. Очень многое объясняет, что скрытое реально происходит в человеке